Written by NexDoor Editorial Team | Reviewed by NexDoor Advisory Team | May 2026

Quick Answer

For most HDB buyers in Singapore, the HDB loan is better if you value stability, CPF flexibility, and no prepayment penalty. A bank loan can be better if you have enough cash, pass the stress test comfortably, and are willing to review or refinance your loan when the lock-in period ends.

The choice is not simply about which rate looks lower today. It is about cash needed upfront, rate risk, MSR/TDSR comfort, refinancing discipline, and whether a changing monthly payment would affect your household.

| If your priority is... | Usually consider | Why |

|---|---|---|

| Payment certainty | HDB loan | The HDB concessionary loan rate is more predictable because it is pegged to the CPF Ordinary Account interest rate plus 0.1% per annum. |

| Lower starting interest cost | Bank loan | Bank packages can be cheaper at entry, but the rate may change after lock-in and needs active review. |

| Lowest cash needed upfront | HDB loan | The down payment can generally be paid from CPF OA, subject to eligibility and CPF rules. |

| Comfort with refinancing | Bank loan | A bank loan works better for buyers who are disciplined about comparing packages before lock-in expiry. |

Who This Guide Is For

- First-time HDB resale buyers choosing between an HDB loan and a bank loan.

- Upgraders who want to understand monthly payment risk before committing.

- Buyers with strong CPF OA balances but limited cash savings.

- Households comparing lower advertised bank rates against long-term certainty.

Key Takeaways

- The HDB loan rate is currently 2.6% per annum, based on the CPF OA rate plus 0.1%. If the CPF OA rate changes, the HDB loan rate can also change.

- Bank loan packages can offer lower initial rates, but rates, spreads, lock-in terms, and penalties vary by bank and market conditions.

- A bank loan may save interest if rates stay below the HDB loan rate for long enough, but the borrower takes on refinancing and rate-reset risk.

- For HDB flat purchases, both MSR and TDSR comfort matter. Do not choose a loan that only looks comfortable at the promotional rate.

- The right answer depends on cash buffer, income stability, risk tolerance, and how actively you want to manage the loan.

Common Mistakes To Avoid

- Choosing the lowest advertised rate without checking what happens after the lock-in period.

- Forgetting that bank loans usually require cash for part of the down payment.

- Comparing only the first 2 years instead of the full holding period.

- Ignoring refinancing legal fees, repricing terms, and prepayment penalties.

- Stretching the loan until the MSR or TDSR test is passed on paper but uncomfortable in real life.

Official checks to make before deciding: HDB housing loan and HFE guidance on hdb.gov.sg; CPF Ordinary Account and accrued interest information on cpf.gov.sg; MAS TDSR/MSR and residential property loan rules on mas.gov.sg.

This is one of the most common questions first-time HDB buyers ask, and one of the most misunderstood. The answer in 2026 is more nuanced than it has been in previous years because bank packages may look attractive at entry, while the HDB loan still offers certainty and flexibility. Here is the honest comparison.

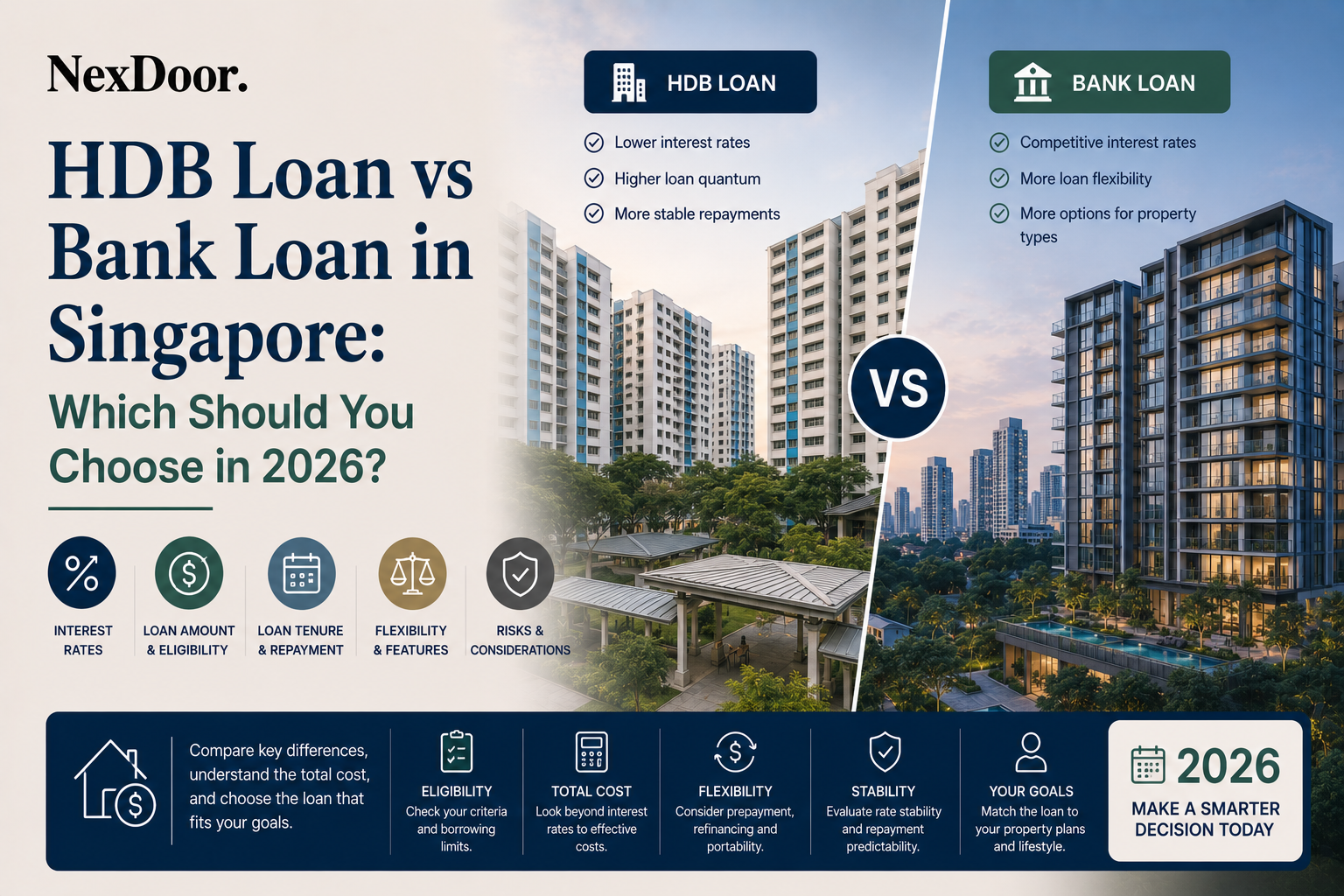

HDB Loan vs Bank Loan in Singapore: The Key Differences

| HDB Loan | Bank Loan | |

|---|---|---|

| Interest rate | Currently 2.6% per annum, pegged to CPF OA rate + 0.1% | Package-dependent. Initial fixed rates may be lower, then usually reset or float after lock-in |

| Rate certainty | More predictable, subject to CPF OA rate movement | Fixed only during lock-in, then may move with the package benchmark |

| Maximum LTV | Up to 75% of flat value, subject to eligibility | Up to 75% of flat value, subject to bank assessment |

| Minimum cash down payment | Often $0 cash if CPF OA is sufficient and rules are met | Usually 5% cash, with the balance from CPF OA/cash |

| Loan eligibility | Requires HFE letter and HDB loan eligibility | Based on bank credit assessment and regulatory limits |

| Prepayment penalty | None for HDB loan prepayment | Penalty may apply during lock-in |

| Refinancing | Can switch to a bank loan later | Can refinance or reprice after lock-in, subject to terms |

| Flexibility | High if you value simplicity and prepayment freedom | Higher effort, because the borrower must manage rate resets |

The Rate Comparison: What You Are Actually Paying

The tables below use illustrative rates to show how sensitive the decision is to interest-rate movement. Before committing, compare actual bank packages, lock-in terms, repricing options, and your own income buffer.

Monthly payment comparison on a $400,000 loan over 25 years:

| Interest Rate | Monthly Payment | vs HDB Loan |

|---|---|---|

| 1.6% (illustrative bank entry rate) | $1,623 | -$277/month |

| 2.0% (illustrative moderate rate) | $1,696 | -$204/month |

| 2.6% (HDB loan illustration) | $1,900 | Baseline |

| 3.0% (higher bank scenario) | $1,903 | +$3/month |

| 3.5% (stress scenario) | $2,011 | +$111/month |

| 4.0% (full stress scenario) | $2,123 | +$223/month |

The crossover point, where the bank loan becomes more expensive than the HDB loan in this illustration, is around 3.0%. If rates stay below that, the bank loan can win on monthly payments. If rates rise above that, the HDB loan becomes cheaper in this simplified comparison.

HDB Loan vs Bank Loan Singapore: Total Interest Paid Over 25 Years

This is where the comparison gets most meaningful, not just the monthly payment, but what you actually pay over the full loan life.

Total interest paid on a $400,000 loan over 25 years:

| Scenario | Total Interest Paid | Difference vs HDB Loan |

|---|---|---|

| Bank loan stays at 1.6% throughout | ~$87,000 | Save ~$82,000 |

| Bank loan averages 2.0% overall | ~$108,000 | Save ~$61,000 |

| HDB loan at 2.6% throughout | ~$169,000 | Baseline |

| Bank loan averages 3.0% overall | ~$172,000 | Pay ~$3,000 more |

| Bank loan averages 3.5% overall | ~$204,000 | Pay ~$35,000 more |

| Bank loan averages 4.0% overall | ~$237,000 | Pay ~$68,000 more |

Total interest paid on a $500,000 loan over 25 years:

| Scenario | Total Interest Paid | Difference vs HDB Loan |

|---|---|---|

| Bank loan stays at 1.6% throughout | ~$109,000 | Save ~$103,000 |

| Bank loan averages 2.0% overall | ~$135,000 | Save ~$76,000 |

| HDB loan at 2.6% throughout | ~$211,000 | Baseline |

| Bank loan averages 3.0% overall | ~$215,000 | Pay ~$4,000 more |

| Bank loan averages 3.5% overall | ~$255,000 | Pay ~$44,000 more |

| Bank loan averages 4.0% overall | ~$296,000 | Pay ~$85,000 more |

The key insight: the bank loan savings are real and substantial — but only if rates stay below approximately 3% for the majority of your loan tenure. If rates average 3.5% over 25 years, you are paying more than you would have with the HDB loan from day one.

The Bank Loan Stress Test: What You Must Run Before Deciding

Unlike HDB loans, bank loans require you to pass the Total Debt Servicing Ratio (TDSR) stress test at a minimum rate of 4%. This means the bank calculates whether you can afford the monthly payment as if the rate were 4% — even though you may be signing at 1.6%.

For HDB flat purchases specifically, the Mortgage Servicing Ratio (MSR) also applies — capping your monthly mortgage at 30% of gross household income regardless of loan type.

Why this matters:

If your household income is $7,000 per month and you are borrowing $400,000:

| Rate | Monthly Payment | % of Income |

|---|---|---|

| 1.6% (actual) | $1,623 | 23% |

| 4.0% (stress test) | $2,123 | 30% |

At 4%, your mortgage payment sits at exactly 30% of income — right at the MSR limit for HDB purchases. This is important: if the stress test payment pushes you above 30% of income, the bank will not approve the loan quantum you are applying for.

The personal stress test rule: If the 4% monthly payment exceeds 30% of your household income for an HDB purchase, the loan amount is too high — regardless of what the bank offers at the initial rate.

The Cash Down Payment Difference

This is frequently overlooked and can be the deciding factor for buyers with limited cash savings.

For a $600,000 flat:

| HDB Loan | Bank Loan | |

|---|---|---|

| Down payment (25%) | $150,000 | $150,000 |

| Minimum cash required | $0 | $30,000 (5%) |

| Can use CPF for | Full $150,000 | Up to $120,000 (20%) |

If your CPF OA is strong but your cash savings are limited, the HDB loan removes the cash down payment requirement entirely. For first-time buyers who have been building CPF but have not yet accumulated significant cash savings, this is a material advantage.

When the HDB Loan Makes More Sense

Choose the HDB loan if:

Your cash savings are limited — you need the 0% cash down payment flexibility

You are risk-averse and want certainty — knowing your payment will never change regardless of global rate movements

You value prepayment flexibility — the ability to make lump sum payments anytime without penalty

You are buying during a period of rate uncertainty and do not want to monitor and refinance every 2 years

Your household income or employment situation has any uncertainty — the HDB loan is more forgiving

When the Bank Loan Makes More Sense

Choose the bank loan if:

You have sufficient cash for the 5% minimum cash down payment

You have a strong emergency fund and can absorb rate increases without financial stress

You pass the 4% stress test comfortably — not just barely

You are financially disciplined enough to refinance at the end of each lock-in period to maintain competitive rates

You plan to sell or refinance within 5 to 7 years — capturing the low rate benefit before rates potentially rise

The Refinancing Reality

Bank loan borrowers need to actively manage their loan — not set and forget.

When your 2-year fixed rate lock-in ends, your loan reverts to a floating SORA-linked rate. This rate can be significantly higher than the initial fixed rate. Borrowers who do not refinance at this point often end up paying more than the HDB loan rate without realising it.

The discipline required:

Monitor your lock-in expiry date

Start comparing rates 3 to 4 months before expiry

Factor in legal fees for refinancing ($1,500 to $2,500) when calculating whether switching makes financial sense

Repeat this process every 2 to 3 years for the life of the loan

If this level of active financial management does not fit your lifestyle or personality, the HDB loan's simplicity has genuine value.

The Decision Framework

| Your Situation | Recommended Choice |

|---|---|

| Limited cash savings | HDB loan |

| Risk-averse, want payment certainty | HDB loan |

| Strong cash buffer, financially disciplined | Bank loan |

| Planning to sell within 5 to 7 years | Bank loan |

| Income uncertainty | HDB loan |

| Comfortable managing refinancing every 2 to 3 years | Bank loan |

| Both partners' income is stable and growing | Bank loan |

The Honest Bottom Line

In 2026, the bank loan offers genuine savings at current rates — approximately $60,000 to $100,000 in interest over 25 years on a $400,000 to $500,000 loan, assuming rates stay below 3%. That is a real number worth taking seriously.

But the HDB loan offers something equally valuable: certainty. You know exactly what you will pay every month for 25 years. You can make lump sum payments whenever you want. You never have to worry about SORA movements or lock-in expiry dates.

The right answer depends on your cash position, your risk tolerance, and your willingness to actively manage a bank loan over time. Neither is universally better — but one will be better for your specific situation.

If you want NexDoor to run both scenarios against your actual income, loan amount, and timeline, we are happy to do it with you before you commit.

Reach out to NexDoor — let's find the loan structure that fits your situation.

Interest calculations are illustrative based on stated rates and loan amounts. Actual bank rates vary by lender, loan quantum, and applicant profile. HDB loan rate is subject to CPF OA rate changes. Total interest figures assume stated rate held constant throughout tenure — actual blended rates will vary. This post does not constitute financial advice.

Sources: HDB.gov.sg; CPF.gov.sg; MAS.gov.sg