Written by NexDoor Editorial Team | Reviewed by NexDoor Advisory Team | May 2026

Key Takeaways

Your maximum loan is determined by TDSR (55% of gross income) and LTV (75% of property value)

Always stress test at 4% — if you cannot afford the payment at 4%, the price point is too high

The fastest a private condo transaction can complete is 8 to 10 weeks from OTP exercise

Completion timeline is one of the most valuable things you can negotiate — use it

Seller's loan status directly affects how quickly they can complete

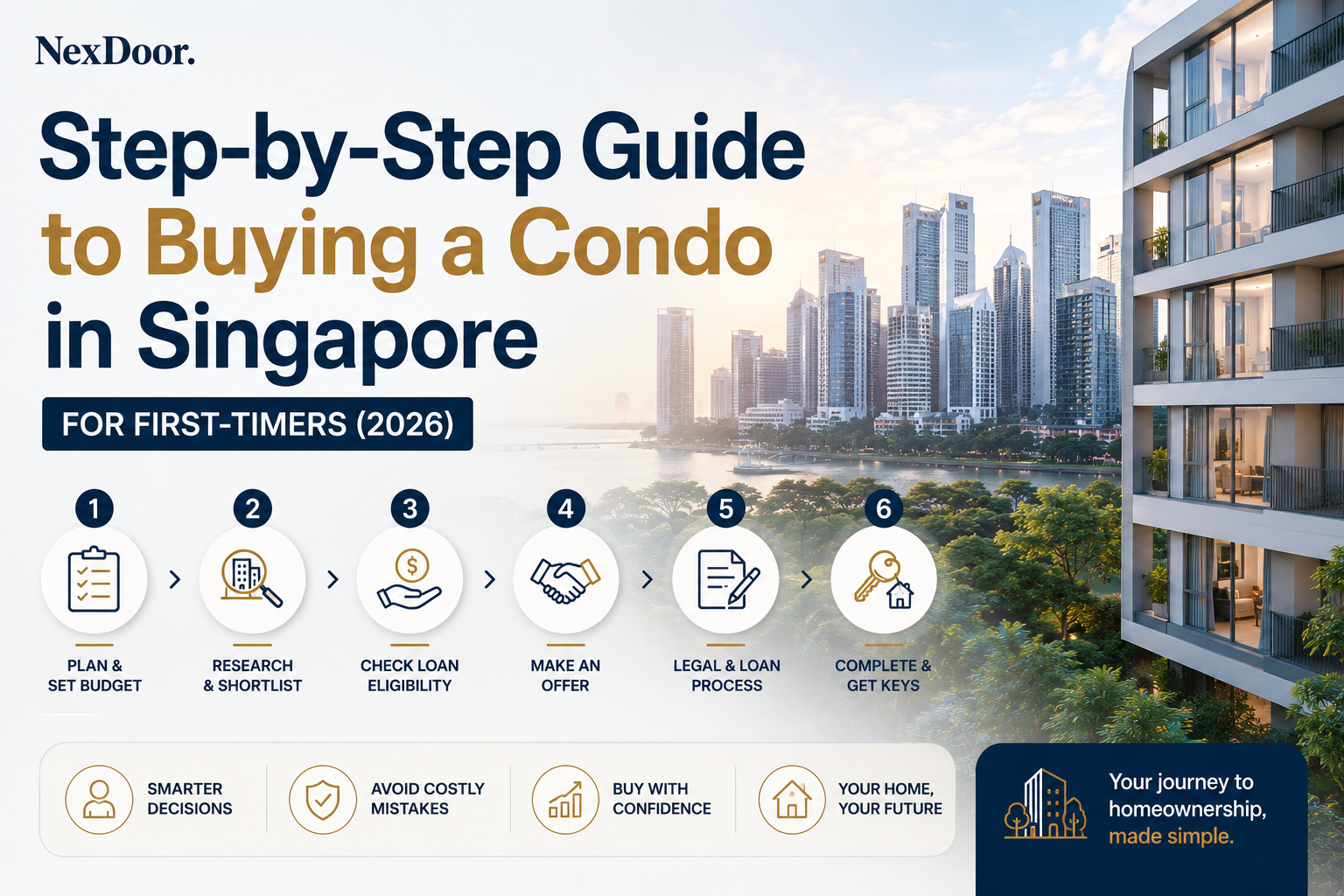

Buying your first condo feels complicated. It does not have to be. Here is everything you need to know, in the order you need to know it.

Step 1: Know How Much You Can Borrow

For private property, two rules determine your loan:

LTV (Loan-to-Value): Maximum loan is 75% of the property price. You fund the remaining 25% from CPF and cash — with at least 5% in cash.

TDSR (Total Debt Servicing Ratio): All monthly debt repayments combined cannot exceed 55% of your gross monthly household income.

Here is what different income levels can borrow, and what that means for your maximum purchase price:

| Combined Income | Max Monthly Payment (55% TDSR) | Max Loan (1.6%, 25yr) | Max Purchase Price |

|---|---|---|---|

| $8,000 | $4,400 | ~$1,028,000 | ~$1,371,000 |

| $9,000 | $4,950 | ~$1,157,000 | ~$1,543,000 |

| $10,000 | $5,500 | ~$1,285,000 | ~$1,713,000 |

| $11,000 | $6,050 | ~$1,414,000 | ~$1,885,000 |

| $12,000 | $6,600 | ~$1,542,000 | ~$2,056,000 |

| $13,000 | $7,150 | ~$1,671,000 | ~$2,228,000 |

| $14,000 | $7,700 | ~$1,799,000 | ~$2,399,000 |

| $15,000 | $8,250 | ~$1,928,000 | ~$2,571,000 |

| $16,000 | $8,800 | ~$2,056,000 | ~$2,741,000 |

Note: TDSR includes all existing debt — car loan, personal loans, credit cards. If you have a car loan of $1,000/month, subtract that from the max monthly payment column first.

Step 2: Always Run the Stress Test

Current rates are at historic lows. Banks offer fixed rates from 1.6% in 2026. But rates will not stay here forever.

Before committing to any price, run the payment at 4%. If that number makes you uncomfortable, the price is too high for your situation.

Here is what the same loan looks like at different rates:

Example: $1,000,000 loan over 25 years

| Interest Rate | Monthly Payment | vs Today |

|---|---|---|

| 1.6% (current 2026) | $4,057 | Baseline |

| 2.0% | $4,239 | +$182 |

| 2.5% | $4,494 | +$437 |

| 3.0% | $4,757 | +$700 |

| 3.5% | $5,028 | +$971 |

| 4.0% (stress test) | $5,306 | +$1,249 |

Example: $1,500,000 loan over 25 years

| Interest Rate | Monthly Payment | vs Today |

|---|---|---|

| 1.6% (current 2026) | $6,086 | Baseline |

| 2.0% | $6,359 | +$273 |

| 2.5% | $6,741 | +$655 |

| 3.0% | $7,136 | +$1,050 |

| 3.5% | $7,542 | +$1,456 |

| 4.0% (stress test) | $7,959 | +$1,873 |

The simple rule: If the 4% payment is more than 40% of your household income, reconsider the price point. You want breathing room — not a mortgage that works only when conditions are perfect.

Step 3: Get Your In-Principle Approval (IPA)

Before viewing a single unit, approach two or three banks for an IPA. This confirms:

How much they will lend you

At what indicative rate

Subject to the actual property valuation

The IPA is free, takes a few days, and gives you a confirmed budget before you fall in love with anything. Do not skip this step.

Step 4: Find Your Unit and Make an Offer

Once you have found the right unit and agreed on a price, the seller issues you an Option to Purchase (OTP). You pay a 1% option fee — negotiable, but 1% of the purchase price is standard for private residential.

You then have 14 days (extendable by agreement) to decide whether to exercise the option.

Step 5: What You Can Negotiate — and Should

Most first-time buyers negotiate only on price. Price matters — but these are equally valuable:

Completion date / timeline This is often more flexible than price. A seller who needs time to find their next place may accept a lower price in exchange for a longer completion. A seller who needs to exit quickly may take less to get a fast close.

Standard completion for private property is 8 to 12 weeks from OTP exercise. You can negotiate shorter or longer depending on both parties' needs.

Inclusion of furniture and fittings Air-conditioners, built-in wardrobes, kitchen appliances — these can be written into the OTP. Sellers often agree to leave items they would otherwise have to remove and dispose of.

Option period extension The standard 14-day option period can be negotiated longer — useful if you need more time to secure your formal loan offer or conduct due diligence.

Vacant possession vs tenanted If the unit is currently tenanted, you can negotiate when the tenant vacates — before or after completion. This affects your renovation timeline.

Step 6: Exercise the OTP and Secure Your Loan

When you exercise the OTP, you pay a further 4% deposit (making 5% total with the option fee). At this point:

Engage a conveyancing lawyer immediately — fees run $2,500 to $3,500 for private property

Submit your formal loan application to your chosen bank — convert the IPA into a Letter of Offer

Pay Buyer's Stamp Duty — calculated on the purchase price, payable within 14 days of OTP exercise. Can be paid from CPF OA after initial cash payment

Step 7: How Fast Can You Actually Complete?

This is where most first-timers get surprised — completion speed depends on both you AND the seller.

Your side (buyer):

Bank loan disbursement typically takes 4 to 6 weeks from formal application approval

CPF withdrawal takes 2 to 3 weeks after bank approval

Lawyer coordination runs in parallel — typically 6 to 8 weeks total

The seller's side — this is the variable:

| Seller Situation | Impact on Completion |

|---|---|

| Seller has no outstanding loan | Fastest — completion can happen in 8 to 10 weeks from OTP exercise |

| Seller has an outstanding bank loan | Bank needs to discharge the mortgage — adds 2 to 4 weeks, typical completion 10 to 14 weeks |

| Seller is also buying simultaneously (contra) | Timeline tied to their purchase — can add 4 to 8 weeks, total 12 to 16 weeks |

| Seller needs extension of stay | Completion happens on schedule but seller stays on — negotiate this upfront |

The realistic minimum: 8 weeks from OTP exercise if the seller has no loan and both parties have all documents ready.

The realistic average: 10 to 12 weeks for most straightforward transactions.

What slows it down: Seller's existing mortgage, missing documents, CPF withdrawal delays, or any legal complications on the title.

Pro tip: Ask the seller upfront — do you have an outstanding loan on this property? Are you also buying another property simultaneously? Their answers tell you immediately how flexible the timeline is likely to be.

Step 8: Completion Day

On completion day:

Your lawyer transfers the balance purchase price to the seller's lawyer

The bank disburses the loan directly to your lawyer

CPF is withdrawn and transferred

Keys are handed over

You are a condo owner

The Full Timeline at a Glance

| Stage | Timeframe |

|---|---|

| Get IPA | 3–5 working days |

| Search and view | As long as you need |

| Negotiate and receive OTP | Day 0 |

| Exercise OTP (pay 4% deposit) | Within 14 days of OTP |

| Submit formal loan application | Within 1 week of exercise |

| Bank Letter of Offer issued | 2–4 weeks after submission |

| CPF withdrawal processed | 2–3 weeks after bank approval |

| Legal completion | 8–16 weeks from OTP exercise |

The Simple Summary

Buying a condo for the first time comes down to four things done in the right order:

Know your budget before you view — get your IPA

Stress test at 4% before you commit — not after

Negotiate on timeline and inclusions, not just price

Ask the seller about their loan and next steps — it tells you everything about how the transaction will flow

The process is manageable. The numbers are knowable. The key is doing the preparation before you fall in love with a unit, not after.

If you want NexDoor to walk through the full affordability calculation and loan stress test for your specific income and budget, we are happy to do it with you before you start viewing.

Reach out to NexDoor — let's make sure the numbers work before you commit.

Loan calculations are illustrative based on stated interest rates and income figures. Actual loan approval depends on individual bank assessment, existing liabilities, and property valuation. BSD calculations per IRAS prevailing rates. Completion timelines are indicative and depend on both parties' circumstances. This post does not constitute financial or legal advice.

Sources: MAS.gov.sg; CPF.gov.sg; IRAS.gov.sg